-

- April 1, 2025

- 0

Uncertainty

It is no exaggeration to say that investing is the art of decision making in uncertain situations. And we are certainly seeing a lot of uncertainty right now. We’ve already discussed the effects of tariffs (TLDR; they are bad), but here we want to look at the uncertainty caused by the administration’s haphazard communications on the topic.

Just some examples:

Jan. 20 (Inauguration Day): Trump says that tariffs on Mexico, Canada and China will be implemented on February the first.

Feb. 1: Trump signs executive order to implement tariffs on Canada, Mexico and China. These are set to start on February the 4th.

Feb. 3: Trump delays tariffs on Canada and Mexico by a month.

Feb. 4: 10% tariffs are put in place against China.

Feb. 10: Trump says he will impose 25% tariffs on steel imports, and he raises aluminum tariffs from 10% to 25%.

Feb. 26: Trump says at Cabinet meeting he might give Canada and Mexico a reprieve on tariffs until April 2.

Feb. 27: Trump says tariffs on Canada and Mexico will start on March the 4th..

March 2: Commerce Secretary Howard Lutnick says tariffs on Canada and Mexico could be less than 25%.

March 3: Lutnick again says it’s possible the tariffs don’t go into effect.

March 3: Trump confirms they will.

March 4: Trump levies 25% tariffs against Mexico, Canada and China. Lutnick says some of the tariffs could be rolled back on March the 5th.

March 5: Trump delays auto industry tariffs until April the 2nd.

March 6: Trump delays tariffs on Mexican and Canadian goods. This reprieve expires on April the 2nd.

I gave up at that point.

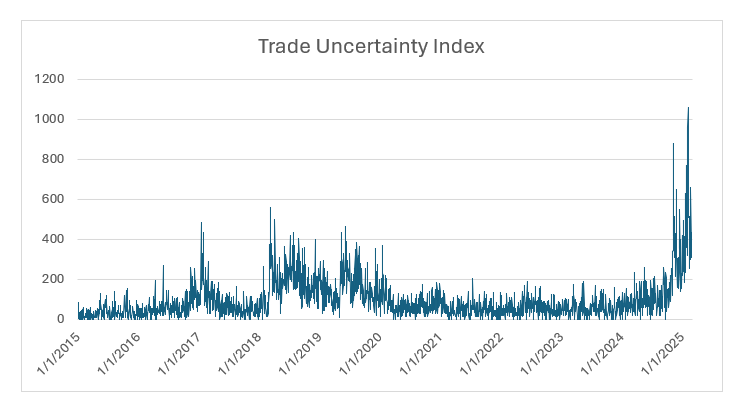

Having a way to quantify this type of this should be useful and an attempt has been made by Caldara et al (2019). They created an index that counts instances of the words that signal economic uncertainty (“tariff”, “import duty”, “import barrier”, “trade treaty”, “trade policy”, “trade act”, “dumping”, “import fee”, “tax”, “foreign goods”, “foreign oil”, “import” ,”imports”, “imported”, “surtax”, “surcharge”, “uncertainty”, “uncertain”, “risk”, “dubious”, “unclear”, “potential”, “probable”, “predict” and “danger”), in seven major US newspapers.

The index is shown here:

There are lots of ways you could use this index in your investing. What follows is just one way.

It doesn’t seem like the levels of the index are predictive. This sort of makes sense because it is obvious that the index stays in certain regimes for long periods. The average during the Trump administration periods is nearly three times the average during non-Trump administration periods.

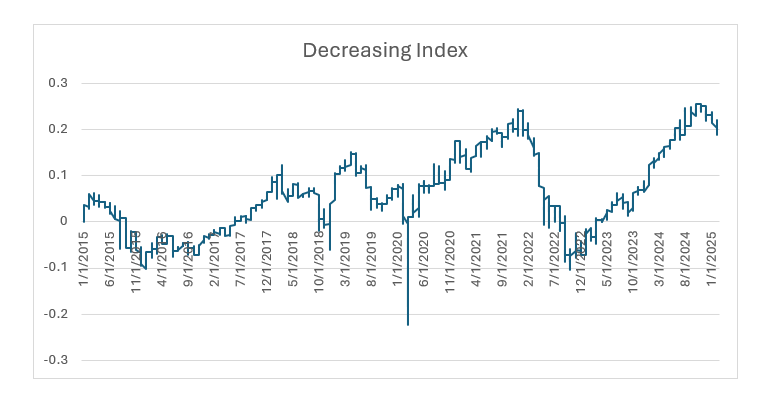

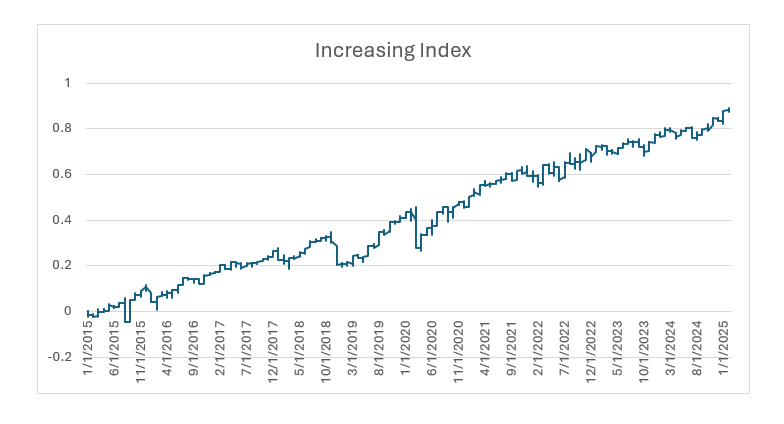

But the change of the index does seem to be predictive.

If we restrict ourselves to index values on trading days (the index is also calculated on weekends and holidays), we find that an increase in uncertainty predicts positive next-day returns. The index seems to capture emotionally driven over-reaction.

The cumulative CAGR for this increasing/decreasing rule is shown below:

This is intriguing, but I don’t trust it. First, we don’t have much data. While we have ten years of daily data it seems more realistic to say we have two regimes: Trump and non-Trump. Next, the signal is very strongly, negatively auto-correlated at the daily level: -35%. And the market itself is also negatively auto-correlated: -14%. It seems possible that the uncertainty index is just capturing this effect.

More analysis is required. But the process of finding usable signals starts with simple observations, and this index seems like it will remain relevant for the next four years at least.

Caldara, Dario, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and Andrea Raffo, “The Economic Effects of Trade Policy Uncertainty,” manuscript presented at the 91st meeting of the Carnegie-Rochester-NYU Conference on Public Policy, April 2019.

Disclaimer

This document does not constitute advice or a recommendation or offer to sell or a solicitation to deal in any security or financial product. It is provided for information purposes only and on the understanding that the recipient has sufficient knowledge and experience to be able to understand and make their own evaluation of the proposals and services described herein, any risks associated therewith and any related legal, tax, accounting, or other material considerations. To the extent that the reader has any questions regarding the applicability of any specific issue discussed above to their specific portfolio or situation, prospective investors are encouraged to contact HTAA or consult with the professional advisor of their choosing.

Except where otherwise indicated, the information contained in this article is based on matters as they exist as of the date of preparation of such material and not as of the date of distribution of any future date. Recipients should not rely on this material in making any future investment decision.

LEAVE A COMMENT